Page Contents

Key Contacts

Related Services

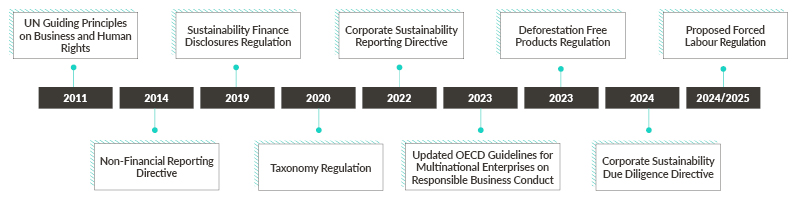

It has been over 10 years since the United Nations (UN) published its Guiding Principles on Business and Human Rights highlighting a corporate responsibility to respect human rights. Following the publication of these principles, there was a societal expectation that companies would act responsibly in the operation of their businesses. Despite this, improvements in corporate behaviour have been slow to progress. This lack of progress has led to an increasing number of countries around the world taking steps to legally require companies to understand the adverse impacts of their operations on human rights and environmental matters. In the first part of this advisory series on business and human rights, we focus on the human rights aspects of the legislative initiatives being introduced and provide an overview of the mandatory due diligence and reporting obligations being introduced in the European Union (EU).

Evolution of human rights reporting and due diligence obligations

Key EU legislative initiatives

Recent legal developments focus on human rights disclosure and due diligence obligations. These are seen as essential components of the sustainability legislation that has been introduced, not only by the EU but also by individual EU member states, the United Kingdom, the United States, Brazil, Japan and Australia. In this section, we provide an overview of the key EU legal developments and practical implications for companies.

Corporate Sustainability Reporting Directive (CSRD)

The legal requirement for companies in scope of the reporting obligations under CSRD is for such companies to report on what, if anything, they are doing in relation to environmental, social and governance matters considered material to their business. Respect for the human rights, fundamental freedoms, democratic principles and standards established in the International Bill of Human Rights and other core UN human rights conventions are identified as a category of social and human rights factors that need to be covered in the sustainability reporting standards provided for within CSRD.

In scope companies are required to report against an initial set of 12 standards, the European Sustainability Reporting Standards (ESRS), which cover various environmental, social and governance topics and will be built on over time. The information to be reported will be included in the sustainability statement, a new section of the directors’ report within the annual report. Human rights matters and impacts are covered by a number of different standards within the ESRS, principally ESRS 2 which is mandatory for all in scope companies to report against and ESRS S1 to 4, being the four social standards which companies will be required to report against if any are considered material to their business.

For example, when reporting on the policies a company has in place in relation to its own workforce (Disclosure Requirement S1-1), a company needs to describe its human rights policy commitments that are relevant to its own workforce. In addition, Disclosure Requirement S1-17 requires a company to disclose the number of work-related incidents and/or severe human rights impacts within its own workforce. Similar disclosure requirements relating to value chain workers, affected communities and consumers/end-users can be found in ESRS S2, S3 and S4 respectively. Forced and child labour are specifically called out as topics to be considered by reporting companies.

In practice, companies, particularly those who wish to be considered best in class, will be keen to show progress is being made to address the adverse human rights impacts of their business operations. Reputational risk and competitive advantage are two of the reasons why businesses will choose to take actions to mitigate against any such negative impacts and to report accordingly.

Corporate Sustainability Due Diligence Directive (CSDDD)

CSDDD will go a step further than CSRD. While CSRD simply requires in scope companies to report on material environmental, social and governance matters, CSDDD will require businesses to take action specifically to identify and address any potential and actual human rights and environmental impacts connected with not only their own operations but also those of their business partners along the company’s chain of activities.

While only the largest companies will be scope of the EU’s legislative requirements, the obligations being introduced mean that these companies need to understand who they are doing business with and to conduct due diligence in respect of their key business relationships irrespective of whether these are direct relationships or not.

From a practical perspective, in scope companies will need to take a number of actions to fulfil their obligations under CSDDD including:

Deforestation Free Products Regulation

The Deforestation Free Products Regulation principally deals with an environmental issue, deforestation. The regulation provides that in-scope commodities including wood, cattle, cocoa, coffee and rubber and certain derivative products shall not be placed or made available on the EU market or exported from the EU unless they are deforestation free and are covered by a due diligence statement confirming this. In addition to setting out obligations to combat deforestation and forest degradation and promote deforestation-free supply chains, the regulation states that the commodities and products have to be produced in accordance with the relevant legislation of the country of production including human rights protected under international law.

According to the regulation, when companies are assessing the risk of non-compliance of in-scope commodities and products intended to be placed on the EU market or exported from the EU, violations of human rights that are associated with deforestation or forest degradation, including rights of indigenous peoples, local communities and customary tenure rights holders, need to be taken into account.

Proposal for Forced Labour Regulation

The European institutions are working to finalise a proposal for a Forced Labour Regulation. Once passed, this regulation would prohibit economic operators from placing and making available on the EU market or exporting from the EU products made with forced labour. Competent authorities will be given the power to investigate any violations of this prohibition and issue decisions that could result in the products being prohibited from being placed on the EU market, withdrawn from the markets if they are already available and disposed of.

Taxonomy Regulation and the Sustainable Finance Disclosures Regulation (SFDR)

In the context of driving investment and financing towards sustainable activities and projects, the disclosure obligations introduced by SFDR and the Taxonomy Regulation need to be taken into account.

While the primary focus of the Taxonomy Regulation is to establish a classification system for determining whether an economic activity is environmentally sustainable (the EU Taxonomy), it also introduces disclosure requirements for those required to report sustainability information in accordance with CSRD or its precursor, the Non-Financial Reporting Directive, and if relevant, prepare disclosures under SFDR. It is a key part of the framework created to drive investment towards sustainable activities. While the EU Taxonomy currently focuses on six environmental objectives, this doesn’t mean that social and governance matters do not need to be considered. One of the four criteria that needs to be satisfied in order for activities to be considered taxonomy aligned focuses on social and governance rather than environmental considerations. This states that the economic activity is carried out in compliance with minimum safeguards. These minimum safeguards[1] are procedures implemented by the company that is carrying out the relevant economic activity to ensure alignment with the OECD Guidelines for Multinational Enterprises and the UN Guiding Principles on Business and Human Rights, including the principles and rights set out in the eight fundamental conventions identified in the Declaration of the International Labour Organisation on Fundamental Principles and Rights at Work and the International Bill of Human Rights. In addition, the Taxonomy Regulation states that when implementing these procedures, companies need to adhere to the principle of do no significant harm set out in the sustainable investment definition in SFDR. From a practical perspective, companies need to evaluate the due diligence processes and procedures that are in place to determine whether they comply with the minimum safeguard requirements.

Separately SFDR applies to financial market participants such as asset managers, insurers and banks in relation to certain products they make available. It is necessary for financial market participants to disclose whether they consider principal adverse impacts on sustainability factors. Respect of human rights is specifically referenced in the sustainability factors definition, meaning that consideration needs to be given to whether any specific information related to human rights matters needs to be disclosed on the company’s website and in the pre-contractual disclosures or periodic reports relating to the relevant financial product.

Concluding thoughts

Respect for human rights should be considered one of the key foundations of a responsible business. The introduction of legal obligations for businesses to conduct due diligence on the adverse impacts of not only their business operations but also their value chain on human rights means it is critical for businesses to understand who they are doing business with and to appreciate the influence that they can have on those further down their value chains. In the next part of this advisory series, we will examine the guidance issued by the UN and the OECD of relevance from a human rights perspective and how this links to the mandatory obligations introduced by the EU.

With thanks to Eric Ehigie for his assistance in the preparation of this article.

For more information in relation to this topic, please contact Jill Shaw, ESG & Sustainability Lead or visit our ESG & Sustainability hub.